The digital transformation of the Polish economy is underway. The National e-Invoice System (KSeF) has the potential to revolutionize document flow, accelerate settlements, and significantly impact the financial liquidity of companies – it also raises many questions. We present a comprehensive guide for companies on KSeF, implementation deadlines, and the most important conditions of the system. Check if your company is ready and take advantage of the support of accounting office specialists in the smooth and safe implementation of KSeF in your company.

Introduction to KSeF

The National e-Invoice System (KSeF) is a central IT platform used for issuing, transmitting, and storing structured invoices. A structured invoice is an electronic document in XML format, compliant with a specific logical structure (schema) published by the Ministry of Finance.

The main objective of KSeF is to standardize the invoice format, streamline tax control, and prevent VAT fraud. From the entrepreneur’s perspective, the system is intended to ensure digitization of processes, easier archiving, and faster settlements.

Legal basis and KSeF implementation deadlines

- The obligation to use KSeF results from the amendment to the Act on tax on goods and services (VAT).

- The legal basis is primarily the amendment to the VAT Act, the implementation of which was preceded by Poland obtaining a derogation decision from the EU Council enabling the introduction of mandatory e-invoicing.

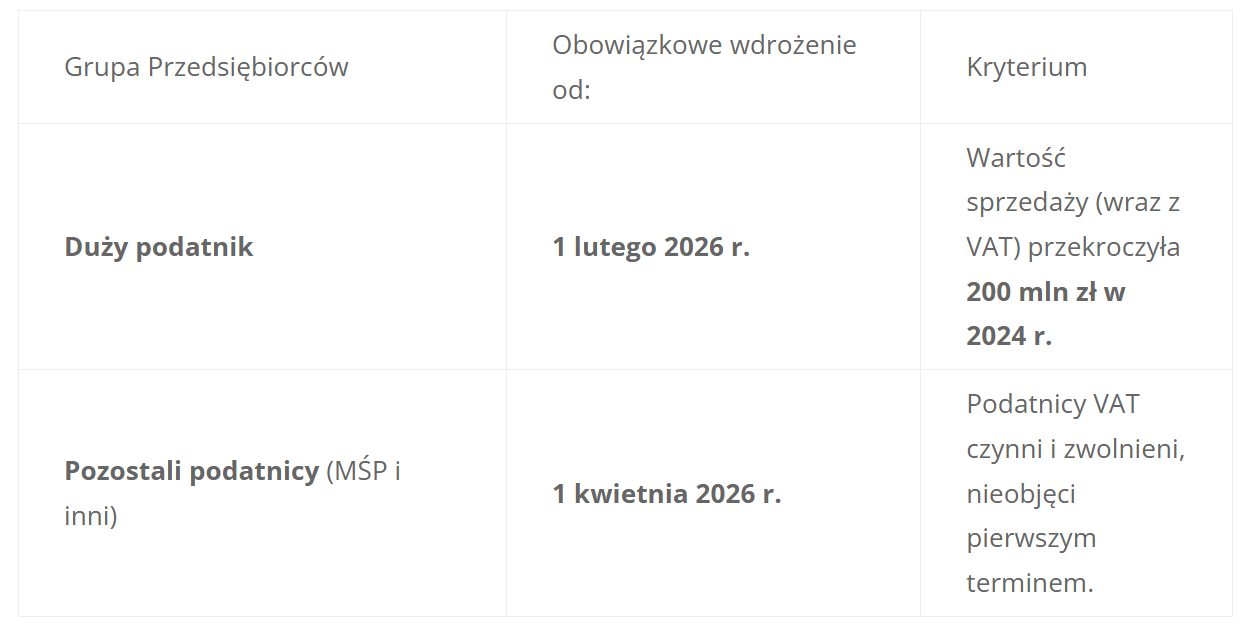

- Effective date for large taxpayers: February 1, 2026, other taxpayers: April 1, 2026.

Current mandatory KSeF deadlines

Following the latest legislative changes, the implementation of mandatory KSeF has been divided into two stages, with a new, postponed effective date.

Exceptions and deferrals:

(e.g., due to small scale of operations or other criteria), the obligation is planned to be introduced from January 1, 2027 (legislative work is ongoing).

it is permissible to issue invoices outside KSeF for transactions with a total sales value in a month less than or equal to PLN 10,000 (this applies to small amounts for taxpayers not covered by digital exclusion).

will continue to be recognized as simplified invoices until the end of 2026.

taxpayers in the sales ledger (JPK_VAT with declaration) will not be required to indicate the KSeF number. This obligation is to enter into force on August 1, 2026.

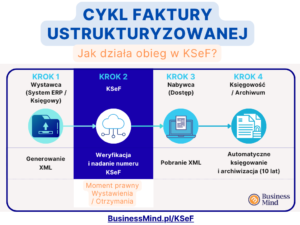

KSeF serves as the central repository for invoices in Poland. The invoicing and document flow process is as follows:

The taxpayer issues a structured invoice (in XML format compliant with the Ministry of Finance schema) in their accounting software or using free MF tools (Taxpayer Application).

The invoice is sent to KSeF. This requires user authentication (e.g., Trusted Profile, qualified electronic signature/seal, or dedicated token/certificate).

The KSeF system verifies the correctness of the invoice schema. If the verification is positive, the system assigns it a KSeF identification number and the date and time of acceptance. From that moment, the structured invoice is considered issued and received.

The invoice becomes available in KSeF for both the issuer and the buyer.

Corrective Invoices

Corrective invoices (“in plus” and “in minus”) must also be issued in structured form via KSeF.

Offline Mode

In case of KSeF failure or the need to urgently issue an invoice, it is permitted to issue it outside the system (in XML, marked with a QR code), with the obligation to send it to KSeF no later than the next business day (so-called “offline24” mode).

Benefits and challenges associated with KSeF

Benefits for Entrepreneurs

Shortened VAT refund period from 60 to 40 days (for invoices issued exclusively in KSeF).

KSeF stores structured invoices for 10 years, relieving the taxpayer of the obligation to archive them independently.

Elimination of the need to send JPK_FA files (for invoices from KSeF) and no need to issue duplicates.

Guarantee that the invoice reached the contractor and was issued by an authorized entity.

Automatic import of invoice data into accounting systems and VAT records.

Challenges and Problems in Practice

The need to adapt or purchase new financial and accounting software capable of communicating with KSeF via API.

Restructuring of internal invoicing processes, document flow, and authorization assignment.

The need to obtain and manage digital authentication methods (signature, seal, token) and grant permissions to employees or the accounting office.

Risk of errors related to the inability to cancel an invoice after it has been accepted in KSeF – any mistakes require issuing a correction.

The need to determine how to handle invoices for foreign entities and consumers (B2C), for whom e-invoicing in KSeF is voluntary.

KSeF and different groups of entrepreneurs

The obligation to use KSeF applies in principle to all taxpayers with a Polish Tax ID, regardless of their VAT status (active, exempt) and legal form.

Large companies

- Due to the large scale and complexity of ERP systems, implementation requires in-depth analysis and system integration already at the planning stage (obligation from February 1, 2026).

SMEs and Self-Employed

- Despite the later deadline (April 1, 2026), adapting systems or switching to MF tools takes time.

- Small companies will appreciate the free tools, but must remember the need for authentication and maintaining continuity of invoicing.

Taxpayers exempt from VAT

- Will be subject to the obligation on the general deadline (April 1, 2026).

Flat-rate farmers and VAT groups

- VAT RR invoices are issued in KSeF by the buyer (VAT taxpayer) only if the farmer submits an appropriate declaration in the system.

- Invoices issued before joining the VAT group remain in KSeF and are available to the taxpayer.

KSeF and VAT and tax settlements

KSeF is closely integrated with the VAT settlement system, introducing significant changes:

A structured invoice is considered issued on the day and at the time of its transmission and acceptance in KSeF (receipt of the KSeF number).

A structured invoice is considered received by the buyer at the moment it is made available in KSeF, not at the time of its physical receipt. This affects the moment when the right to deduct VAT arises. Corrective invoices "in minus" (reducing the tax base) are included in the settlement for the period in which the buyer received the corrective invoice in KSeF.

Invoices from KSeF are automatically verified and visible to the Tax Administration, which is ultimately intended to simplify control processes and eliminate the need to generate JPK_FA.

The obligation to provide the KSeF invoice number in the transfer message for payments in MPP is to be deferred until August 1, 2026.

KSeF and accounting systems.

Most convenient for large and medium-sized companies. The ERP system or accounting software is adapted for automatic communication with KSeF (issuing, receiving, downloading KSeF numbers). This requires software updates and often a dedicated KSeF token.

are free solutions for smaller entities. They enable manual issuing and sending of invoices, as well as their receipt and transfer of data to VAT records (e-microfirm).

How to prepare for KSeF

Most common errors and problems with KSeF in practice

During the implementation period, entrepreneurs may encounter typical problems with KSeF:

Lack or incorrect permissions

Persons responsible for invoicing must be granted access to KSeF, and the accounting office must have appropriate powers of attorney.

Errors in the XML schema

The invoice must be issued in a format compliant with the current MF logical structure. The system will reject a file with incorrect or missing fields.

Delayed transmission

Despite KSeF failure, invoices issued in offline mode must reach the system no later than the next business day.

Lack of KSeF number in payments

From August 1, 2026, the lack of a KSeF number in a transfer under MPP will be an error.

The future of KSeF and digitization of settlements

The implementation of KSeF is one element of a broader digital revolution in the Polish tax system, aimed at full automation of processes. In the coming years, further improvements and integration can be expected:

- The ability to send invoices with attachments (after submitting an appropriate notification in e-US).

- The ability to integrate data from KSeF directly with reporting and financial analysis modules (Business Intelligence), which will increase internal transparency.

KSeF is a tool that, over time, will cease to be just an obligation and will become a support for business in financial management.

Sanctions for entrepreneurs

Penalties for lack of KSeF

– amount and transitional period

Although the new regulations postpone the deadlines, sanctions are provided for failure to comply with mandatory KSeF, aimed at disciplining the market.

Amount of penalties

Generally, penalties will be imposed in the amount of up to 100% of the VAT amount on the invoice, but not less than PLN 1,000 or PLN 500 (for failure to issue a structured invoice or for errors in emergency mode).

Transitional period without penalties

The government plans to introduce a transitional period during which penalties will not be imposed or will be significantly milder.

Entrepreneurs can expect that sanctions for failure to fulfill KSeF obligations will begin to be applied with a delay in relation to the date of mandatory entry of the system.

It is worth following official MF communications – the exact date for the start of imposing penalties is a matter of ongoing legislative work.

KSeF from the entrepreneur's perspective – emergency procedures, credit notes, invoices for consumers and foreign entities

KSeF failure and offline mode: What you need to know about emergency procedures?

Despite the advancement of the system, in case of its unavailability (failure), the regulations provide for special procedures. It is crucial that the entrepreneur knows how to maintain continuity of invoicing and settlements without risking penalties.

In case of failure, you can issue an invoice outside the system (e.g., in your software), but it must comply with the XML logical schema and be mandatorily marked with a QR code.

An invoice issued in offline mode must be sent to KSeF immediately, but no later than the next business day after its issuance.

Despite the delay in transmission, the date of issuance of the invoice is the date on which it was actually prepared outside KSeF.

How do permissions in KSeF affect the work of the accounting office?

KSeF dramatically changes the relationships and working mechanisms between the company and its accounting office. The client is obliged to grant appropriate permissions to their accountant.

You can do this online (if the office has a qualified seal/signature) or by submitting the ZAW-FA form to the Tax Office, indicating the Tax ID of the office or its employees.

The client can grant permissions to: issue, access invoices, and also (importantly for external offices) manage permissions.

Granting permissions is the only legal way in which the accounting office will be able to download purchase and sales invoices for settlements. There is no longer any question of "sending emails with invoices" for B2B accounting purposes.

KSeF and corrective invoices and credit notes: Rules of mandatory e-invoicing

Changes in KSeF directly affect the correction process. It is worth remembering one rule: if the original invoice was issued in KSeF, the correction must also go to KSeF.

Must be issued as structured invoices in KSeF. The system automatically links the correction with the original document, which is important for the moment of VAT deduction ("in minus" – at the moment of receipt in KSeF).

Credit notes, used to correct minor errors by the buyer (e.g., in the address), are not and will not be issued in KSeF. They remain in circulation outside the system (e.g., by email or paper) and are subject to existing regulations.

KSeF and B2C invoices (for consumers) and foreign entities

The obligation of e-invoicing applies only to B2B (Business to Business) transactions in Poland (and partially B2G). In the case of consumers and foreign entities, special rules apply.

Issuing e-invoices in KSeF for natural persons not conducting business activity remains voluntary. It will still be possible to issue a paper or electronic invoice (e.g., PDF), which should be delivered to the consumer in an agreed manner.

Invoices for foreign contractors who do not have a Polish Tax ID (even though they are subject to Polish VAT) also do not have to be issued in KSeF. The invoice is delivered in an agreed form (e.g., email).

Three Facts about KSeF that are rarely discussed

Although many companies focus on the basics, it is the details that determine trouble-free implementation. Here are three rarely discussed but crucial aspects of KSeF that have enormous practical significance:

Calculating the payment date from KSeF, or the end of "delivery delay"

Self-billing after the new: The issuer is KSeF, not the buyer!

No possibility to cancel an invoice – consequences for pre-invoices and advances

Frequently Asked Questions - FAQ

Support for companies in preparing for KSeF

Mandatory KSeF will enter into force for large taxpayers on February 1, 2026, and for the rest on April 1, 2026. This change requires thoughtful reorganization of processes and investment in technology and work reorganization, but offers real benefits: faster VAT refund, secure archiving, and accounting automation. The key to success is early preparation, analysis of current processes, and ensuring necessary permissions.

Do not delay implementation. Contact Business Mind specialists >> together we will plan a safe and effective integration of your company with the National e-Invoice System.

Contact us

We'll be happy to answer your questions - we know how to provide effective accounting services for companies.

Error: Contact form not found.